| The NYSE's clearinghouse in 1898, six years after its founding |

Traditional financial systems often get mocked for being slow. In North America, for instance, securities markets have recently switched from T+3 to T+2 settlement. Before, if you sold a stock the cash would only appear in your account three days after the trade—now settlement has been moved to a blazing fast two days. In an age where mail is transmitted in milliseconds, this delay seems terribly old fashioned. Or take automatic clearing house (ACH) payments in the U.S. Earlier this month the ability to make same-day ACH debit payments was rolled out, an improvement over the three or four days they used to take, but still no where near immediate.

The snail-like pace of securities and ACH settlement is often contrasted to real-time settlement, say like how payments using banknotes, coins, or bitcoins are finalized the moment the token leaves ones wallet and enters the destination wallet. Or take real-time gross settlement systems operated by central banks, over which a transfer of balances from one account to the other occurs instantaneously and is irrevocable. In the case of securities settlement, why only go from T+3 to T+2? Why not go straight to T+0?

Don't be beguiled by settlement speed. Slow isn't necessarily a bug—it's often a feature. Imagine the following scenario. You and your friends play poker every day at a cafe. To buy into the game, cash or bitcoins are required. And at the end of each game, cash or bitcoin is paid out to the winners. The problem with this system is that each day all players have to lug a transactions medium to the cafe and back from it—and this involves a sacrifice. Banknotes and coins take up lots of space and can be easily stolen. Like bitcoin, they don't yield interest—so a stream of interest income is being foregone to play poker. Once the game is done, the laborious process of counting out cash and banknotes occurs. In the case of bitcoin, the payouts are costly since each one involves incurring a fee to send bitcoins from one wallet to another.

Participants in financial markets have adopted a time-tested strategy to avoid much of the work involved in repetitive use of transactions media like cash: substitute them with IOUs that are only settled from time-to-time. Returning to the poker example, rather than stumping up cash each game players can buy-in using IOUs denominated in cash or bitcoin. These IOUs are recorded in a ledger. Rather than cashing out at the end of the game each player's balance is held over to the next day, only to be updated subject to that day's results. These ledger balances continue to be updated at the close of each game until after (say) the tenth game, everyone finally decides to settle their accounts, upon which all debtors, or losers, bring cash and/or bitcoin to the cafe to pay off winners, or creditors. The system has settled—not in real-time—but T+10.

The advantage of delayed settlement is that quid pro quo is achieved with one set of transactions conducted at the end of the 10-game cycle rather than a set of transaction for each game. No more tedious counting out coins each day or daily bitcoin fees. Because the obligation to carry around cash is kept to a minimum, interest income needn't be sacrificed by players. Nor are there any nuisances of storing cash.

While slowing down the system reduces the amount of work that must be done, it comes at the expense of flexibility and safety. One of the benefits of a cash payment is that transactions media are immediately available for use in subsequent transactions. If a player can only get cash out of the game after ten games, they will have to be sure that they don't need that cash for other payments in the interim. Slowing down the system also introduces credit risk into the system. Players may be unable or unwilling to honor their IOUs at the end of the cycle. Lengthening the cycle only increases the odds of settlement failure due to insolvency or bankruptcy.

If the benefits that your friends expect to harvest from delaying poker settlement—the reduction in work and fees—outweigh the aforementioned costs, then a T+10 system makes a lot of sense. Keep this in mind whenever you encounter a real-life financial transaction like an ACH payment that takes a long time to settle. The system's sluggishness may be designed that way because the conservation of work and transactions costs outweighs the inconveniences of not having immediate availability of transactions media and exposure to credit risk.

Even the bitcoin ecosystem has adopted various forms of delayed settlement. Thanks to high fees and long wait times, Bitcoin companies have been avoiding direct exchanges of bitcoins among each other in favor of netting out bitcoin-denominated IOUs, says Izabella Kaminska, only settling net amounts after some time has passed. And Bitcoin developers are working towards introducing something called the Lightning Network, which will allow users to make payments using fully-backed bitcoin depository receipts rather than having to settle trades directly on the blockchain using regular (and peskily-slow) bitcoins.

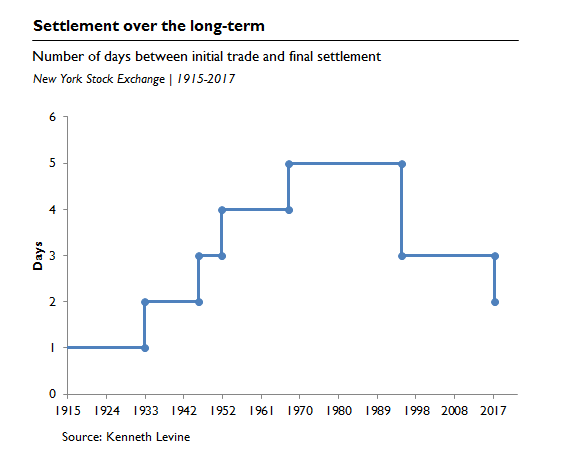

Let's finish off by revisiting the recent shift from T+3 to T+2 securities settlement in the US and Canada. Interestingly, if you zoom out you'll see that over time the New York Stock Exchange shows a predominant tendency to lengthen the settlement cycle, not shorten it. The recent move to T+2 only brings the exchange back to the same settlement speed at which it operated at from 1933 to 1952. Prior to 1933, next-day settlement, or T+1, had been standard.

The lengthening of the cycle to T+2 in 1933, which corresponded with an increase in stock trading volumes, was implemented to "ease the work" of brokerage clerks. Back then all securities were recorded in physical form, so settlement required the transportation by hand of certificates from one office to another by an army of runners. In the face of growing trade volumes, the only way to maintain T+1 settlement would have been to do much more work, which meant hiring more clerks and runners—costs that would be offloaded onto clients. Slowing down the system to T+2 from T+1 presumably would have kept things cheap.

The 1968 switch to T+5 settlement was an effort to cope with the famous "back office crisis." Investors who were too young to remember the Great Depression had begun to arrive in droves to equity markets in the early-60s. Back office clerks could not keep up with amount of work required to settle trades. At one point the NYSE even closed on Wednesdays to help deal with the backlog.

The recent move back to T+2 means that cash will appear in investors' accounts 24 hours earlier, making it easier for them to meet subsequent payments deadlines. Credit risk is reduced too. Brokers conduct trades with other brokers on behalf of their clients, building up credit and debits over the settlement cycle. The shorter the cycle, the quicker these debts will be unwound by transfers of stock and cash, the resulting savings hopefully flowing through to customers.

Why not go straight to real-time, or T+0? The move from T+3 to T+2 means one less day over which brokers can 'net out' their respective debits and credits so as to conserve on transactions costs. T+0 means no netting-out window whatsoever—and that would impose a terrific amount of work on the system. Like I say, it's a trade-off. Real-time settlement is no panacea.

P.S. Here's a great article on the history of securities clearing and settlement: Was Trade Settlement Always on T+3? A History of Clearing and Settlement Changes, by Kenneth Levine (1996)